Two Sides of FI dropped a latest video where the two host Eric and Jason provided transparency over their personal situation.

Are We Hiding Something? Our Real FIRE Portfolio + Expenses

This seem to be a rather odd video because I thought Eric and Jason produced really good content. Their discussion often brings up deeper considerations of financial independence that you don’t get in other FI content (and I used to consume a lot of these content.)

Then I realized they been called out by this Duane guy, who made a content asking more of these YouTube FIRE content producers to be more transparent:

To a certain extent, some people on Reddit might agree with Duane:

I have some thoughts regarding whether we, those people that is writing about this in the community should be more transparent.

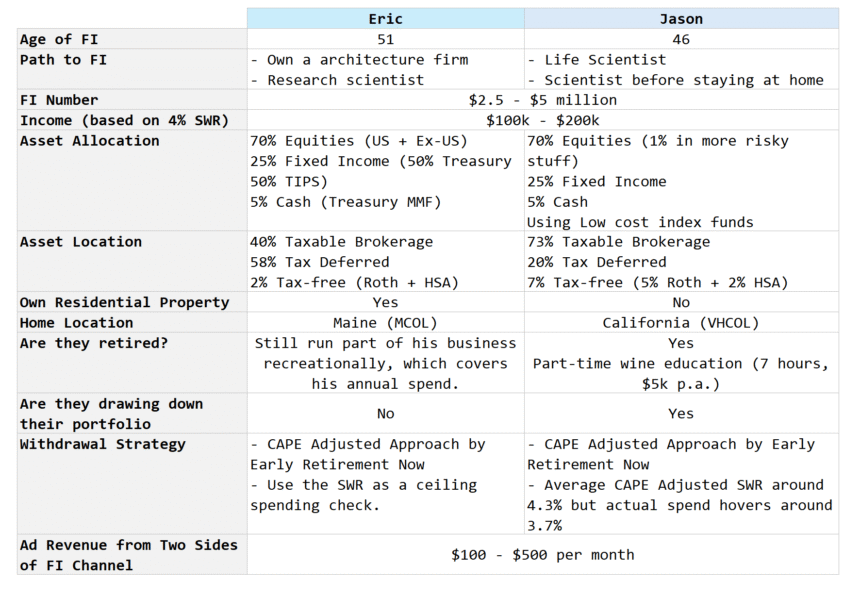

But here is the summary of the “transparency” the two host of the Two sides of FI:

I like this list and this might be a blueprint for you to consider when you are thinking through whether you are financially independent when your numbers are substantial enough.

They did not give their exact numbers, but does satisfy what Duane wants, which is to let people know what is the range of their FI numbers. But as Eric from Two Sides of FI says, knowing the FI number is less important than the spending.

Which is why they explain that their number is based on a 4% SWR strategy which pins the income need that they work with to be $100k to $200k range.

The asset location information is refreshing because while the community discussed the numbers, I don’t have a clear impression how the breakdown based on location can be.

Both of them have much less in the tax-free Roth and HSA accounts than I originally thought. This surprised me a little given that these are the priority accounts that you should try to contribute to if you can. It goes to show that the annual maximum to contribute to these accounts are not so high. Most of their money is in taxable accounts, which means that investing in dividend paying stocks is less efficient.

Whether they own or not own their primary residential property is also important to me because rent can be a rather inflexible spending item that you might need to be more conservative about. The same is whether you are living in a medium cost of living (MCOL) area or a very high cost of living area (VHCOL)

What is the withdrawal or income strategy used?

Both prefer a CAPE-adjusted safe withdrawal rate strategy (SWR), which is a strategy popularized by Karstan Jeske of Early Retirement Now. The CAPE stands for cyclical adjusted price earnings, which is a valuation metric of the US equity market. It is unique in that the earnings is the average of the past 10 years. This makes the valuation number generated to be more “slow changing”. If the CAPE is high, it means that we might be retiring into an environment that are higher in valuation, relative to history.

The safe withdrawal rate that will come up with is lower, which means to retire, you need to set aside more capital. The opposite is also true if the CAPE leans more towards historically low. The evidence show the level of CAPE has a strong correlation to the income survival rate for a fixed income tenure.

A CAPE-adjusted safe withdrawal rate strategy is considered a more variable withdrawal strategy, which means their income will tend to fluctuate a little. I like what Eric shared about where the CAPE-adjusted SWR lands upon the last few years (4.3%).

And also how to read the SWR which is an income ceiling, or the highest income that is recommended not to exceed. You don’t have to keep strictly to it and can spend less, but what is computed is an income recommendation.

Jason still has income from the business that he is running, which covers his spending so he is not drawing down his portfolio while Eric is.

Finally, both of them show just how much income they are making from their 30k subscriber channel.

It probably answers this question:

Now lets get to the part about transparency.

Reasons for More Numbers Transparency from FI/FIRE Content Providers

I will save you from watching Mr Retire with $500,000, or Duane’s video on why he calls for more transparency by listing them out.

He basically hopes major FI content sites like Two Sides of FI can:

- Tell us how much you got if you want us to listen to you.

- What is the ballpark net worth you have? Can I even relate to you?

- Are you even retired yet? Are you experiencing what you are telling us to do?

- What are you invested in? Are you invested in the stuff that you want us to be invested in?

- How about the sponsors in your channel, do you really believe in the sponsors you want us to buy?

- When things you do don’t turn out right, let us know! You make mistakes, that helps a lot for us to know.

And here are the main reasons why greater transparency is good:

- So that we know if we are watching a channel that matches up to what we are looking for

- There are people with $5 million and they may be asking you to invest in something that they invest in. But they have so much higher margin for error relative to the size of their investment. These people might not have so much to lose but some of their viewers might.

- If you are not transparent, how do you expect people to trust what you are saying.

- It is clear communication.

- Promotes Ethical behavior.

- Promotes Accountability.

- If you are transparent, it will improve the decision making process of your viewers

I won’t go into all the points, but I generally agree with most but also want to explain why you might not get what you are looking for.

1. It is the Income Need to Portfolio Value Ratio (or the Safe Withdrawal Rate) That is Most Important to Disclose

What Duane called out was to give a ballpark figure of the number that you are retiring with. If it is $500k, $1 mil or $10 mil.

But that is so much less important because that number is useless without considering a few things:

- What is your income needs or how much you are thinking of spending?

- Related to #1, how is your desired retirement lifestyle or FI lifestyle look like?

- Are you paying for rent or not?

- Do you have other income streams beside this main one that drives the portfolio?

This is where Eric is right.

Many people think that once they reach a certain figure $X,XXX,XXX they might be close to FI. They could be correct.

But I seen too often on my SGFI Subreddit questions like “Can I FIRE Yet?”

They will post long, long breakdown of their assets their liabilities.

Then they leave out what the lifestyle they want and how much it cost them.

It is as if you expect that if you reach $2 million you can retire.

The major part of your money is suppose to provide an income so that you can live a certain lifestyle, but if you don’t know what kind of lifestyle you wish to provide for, and how much it cost, then how do we tell you if you can FIRE?

In my community, many have learn from me and ask: “If you take your income need, divide by the money that you plan to provide the income, what is the ratio?”

Or some would outright ask “What is your SWR?”

That one number be it 6%, or less than 2% tells us a lot of things.

If your number is:

- 6%: We know that your income setup might work in some sequence of future outcomes, but historically there are challenging inflation, deflation and market sequence that you might run out of income prematurely. It also shows us that you have no buffer.

- Less than 2%: You have a lot of money relative to your needs such that even if some of the most challenging situations befall your portfolio, you should be okay. The asset allocation matters much less and what would make your plan work is that your portfolio can drop by half and you will be okay. You basically have 2 times your normal income needs.

This ratio relates the lifestyle with the portfolio capital. There is a lot of rigor put in place with the Safe Withdrawal Framework (You can read Why the Safe Withdrawal Rate (SWR) is Essential for Your Financial Independence) such that we can have a higher degree of confidence the range of whether we will run out or not run out of money prematurely.

If we know this, we can then continue the conversation about a plan is risky or not.

A person with $500k might not look so risk if realistically the lifestyle spending is so much less.

Most importantly, it also lets us know if this content producer is sharing with us a risky plan that they themselves don’t even know it is risky.

2. Yet the Absolute Portfolio or Net Worth Number is Important to Disclose

Duane is right to a certain extend because we want to watch or read content that may be more relatable to us.

As content producers, we will create content closer to our personal situation.

Not just that people want to experience feelings, security, or the lack of security that they can relate to.

And lifestyle.

A person working with a $5 million lifestyle is very different from one with $500,000 lifestyle.

I seen this in my community. Sometimes I will automatically blank out some discussions because i am not of that lifestyle range and I am sure some of my readers as well.

I want to read or view the ones with $5 million lifestyle occasionally but not all the time. I want to regularly stay in tune with those with a lifestyle closer to mine (which is the low range).

3. “Are You Even Retire Yet?” is a Very Valid Question Because the Security of a Working Paycheck Affects Your Emotional Financial Security in Your Plan

I kind of agree with Duane with this question because there are some aspects of FI that you might be more in tune with if you are a retired person.

I am still working, but I think I have some awareness that there are some “meta” or inner data that you will only know well enough if you stop taking a working paycheck.

I can try my best to accept there exist these things that I could only experience if I stop working and imagine/wargame as best I can as if I am in that scenario.

But I have not stopped taking a working paycheck.

The feeling is quite different.

I felt that many (perhaps me included) don’t dare to admit that they don’t dare to retire because they have insecurities with the portfolio income stream they constructed by themselves.

So they choose to keep working.

But yet we can be seen like talking a lot of theories about income, withdrawals and what not.

Sometimes, the folks like my friend STE would subtly called me out by asking me if people spend based on the SWR by selling units. I think he is right to call me out.

And this is where Duane is right.

Some talk big and you wonder if they are generating content just to be able to sell ads or affiliate income.

I can only try my best to be more in touch with my true feelings and securities. This is because ultimately if I am serious about buying an income stream that fits a certain lifestyle, what is the use of lying to myself that my strategy is robust when deep down there are major question marks about it.

This is one of the reasons why I switch from a dividend income strategy to plan the starting capital to a more conservative safe withdrawal rate strategy.

But those who retire will let you know if an actively managed portfolio is harder or easier to manage, whether selling units is actually psychologically tough or can be trusted.

I think in a way, I do see some comments on Duane’s video: “This is why I don’t trust financial advisers”

Which is true because many DIY people also don’t trust them.

There are valid points in that the people that help you plan have not experienced retirement yet, so are they really the best people to help you plan?

This can be a touchy subject because my coworkers help their clients plan for their retirement.

But the truth is partly… the clients also don’t have a choice (which I will go into later). More importantly, those that are not retire need to recognize what we might not get about retirees.

We need to recognize the critical emotional and tangible considerations that we may overlook because we have not experience an extended period of greater freedom and not having a reliable paycheck from work. Try to consider from a position without the safety and comfort of a regular paycheck.

4. Your Affiliate Income or Alternative Income Affects Your Emotional Financial Security in Your Plan

Duane called out the content producers to disclose the affiliate income or ad revenue with good reasons because if you write about retiring and not having a working paycheck, how does the income you earn from the content you provide feature in all this?

This dovetails around what we discuss in the last point. Your securities and emotions might be different without a secure paycheck and one from portfolio income.

I think it’s not just what they earn from their YouTube or affiliate but some might have income coming in from other secured sources.

And some have assigned financial security that helps them deal with it emotionally because of that.

I won’t be surprised some have assigned financial security because they are the only child knowing they will inherit their family’s wealth when they passed away.

I don’t think an exact figure is important but the degree do matter.

Just like the example Eric brought up: If you make content regarding Lean FIRE, and you bring in $2000 monthly from your channel, what gives you your emotional financial security?

Your portfolio income plan or the YouTube income when considered?

The thing about income from these side hustles is such that for some of us, the income is less trusted if you see how volatile it can be. Most in this field after a while kind of know they will bring in a floor amount, but when it comes in is a bit uncertain.

Kinda feels like dividend income.

But this is good color for us to relate to you. If you have a nice old auntie that happens to give you $500 a month, and it does give you emotional financial security, then it’s good to acknowledge that.

5. Just Because You Cannot Relate To Me Doesn’t Mean What I said is False.

Somewhere last year, I saw someone share a link in a Telegram group about Fed might be on track to lower the interest rates. So I made a comment from my observation that “The 10-year Treasury yield seemed to be heading higher lol.”

The person commented that the downtrend is clearer from the Fed. The Fed will find it harder at this juncture since they have shown their hands and the descent is more gradual.

Someone else asked the significance of the longer maturity rate and I explain that the Fed usually controls more of the shorter maturity rates but the longer maturity rates might be determine by more things. And usually debt heavy assets like the REITs borrow cost is more related to the longer maturity yield. And there are more considerations such as the future growth, inflation, you name it.

Most of us see it better today now that the 10-year yield hasn’t come down (as of Jun 2025) due partly to the reasons that I explain.

But what bugs me is that the person seem to think that just because I don’t have any REITs, I have no vested interest, then my views should be questioned.

Which is a problem I have with this degree of vested interest thingy.

We see enough in the comments that people feel “trusted” if the person has more vested interest.

I have news for everyone.

If I have $10 mil and I happen to put all in one stock, it doesn’t mean my analysis (read forecasted opinion) of the stock will make the stock a success. In fact, it might just show I am reckless enough to be so concentrated, betting the money that is important to me, in a way that I really don’t have to.

I learn from my behavior that when a person declares a large vested interest whether in:

- An investment strategy

- A particular security or group of securities

- An income strategy

I will take notice and become curious about the thought process.

Beyond that, there has to be some sensible logic to how we evaluate things.

Just because we don’t have enough vested interest doesn’t mean what we say is without rational or is incompetent advise.

Here are a few cheeky non-vested areas of income planning that is likely correct:

- Your rental income is going to be volatile.

- The aggregate dividends you receive annually is going to be volatile.

- The payout from your income fund is going to be volatile.

- If you think market returns drive your income, there might be periods of market return that make you question if you can have the same income.

Most of these I don’t have vested interest and you can tell me if I am correct or wrong.

6. You Need to Realize Some of Us Have a Face and Real Life Identity Assign to the Numbers

Eric and Jason is right that while you all want transparency, you do realize that we are actual identifiable human beings and different people have different circumstances and will have to deal with these things differently.

It is not only whether you are comfortable but you got to think that your spouse has to deal with it (because your identity is public.)

So what you observe is… those people who keeps their identity show their figures, those who are public with their identity doesn’t show the figures.

I think sometimes it is also easy for you guys to ask for transparency because you could share your situation but your identity is behind a nick or an online profile.

Then again, sometimes I think this is the exchange you might need so that people would follow you.

7. There is always a way to be less authentic.

Finally, you can’t see where my emotional financial security is at and I can’t see yours.

Sometimes, the less introspective people can’t see their own clearly.

A FI or FIRE content person will have their means to not share something, especially the stuff that give them the deepest security. Could be in the event of anything, there are always the bank of mom-and-dad. Or an inheritance. Or a deliberate sizable undeclared income stream.

Try as you might, it is difficult for most to uncover.

But don’t you sometimes find it interesting as a viewer or a reader to be guessing? If everything is declared, then there is nothing for you to guess isn’t it lol?

My Final Thoughts

While I am a content creator, I also consume content as well.

So I see a lot of validity in the things Duane brought up. Yet at the same time, supporting transparency means that I have to do the same thing.

I think I am transparent enough that I am comfortable with. I think those who know where to look can piece the numbers together since I regularly post my monthly spending on my Instagram and you know where my portfolio is.

Beyond that, it’s private.

I think Duane’s point is there should be enough info so that we can have a meaningful discussion and I agree with that. Even if it is not on a YouTube, or blog, I find the lack of a certain degree of transparency affecting the discussion because how a person feels about a certain situation may be related to their own situation. Without that, it is difficult to discuss.

And I think the SWR make it really simple that you don’t have to share much capital as well.

Someone recently share that her number is less than 2%. That is good enough to start because we would know technically if this person belongs to the folks with a risky plan or a very conservative plan.

But at times, you do have to see if we provide you with enough tools to advance your path to FI/FIRE.

I think those who are not fully invested can still provide thought provoking ideas that made you look at things in a different light.

I believe in the long run, those who disagree with me and don’t see value in what I provide, whether is due to the lack of transparency or lack of expert opinion, will just go away. But what is less said is that some of my peers build their audience because they want well crafted and presented content as well.

While transparency is good and vital, that may not be what everyone is looking for. And hence we have more successful FI content people and less successful ones.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.