One of the spending needs that many of you would consider as part of the income needs for your financial independence (FI) or FIRE, is to have enough money for some of the “better things in life”.

Many felt that even if you have the capital to provide a recurring portfolio income that provides for a basic life that is not good enough.

What for do we work so hard only to live a bare minimum life?

They would measure the quality of life they wish to save for, with their current quality of life. A quality of life that they live on a recurring basis. If they feel satisfied with spending $7,000 a month on everything then this is the lifestyle they should FIRE with.

It should not be a surprise that even if they reach a capital close to this originally (let us use a 3% safe withdrawal rate as a rule of thumb for discussion and say the capital needed is {$7k x 12}/0.03 = $2.8 mil), they may feel inadequate.

This is because as life changes, especially with kids:

- There are experiences that need to be paid that they forgot to consider previously.

- They are not sure how many of these experiences they have missed out, so they might need more income.

- Things seem to cost more nowadays.

Because we all view that we needed these experiences every year, we will need a greater recurring income stream, which if you use that rule of thumb of 3% means an ever larger capital.

I think there is another way to consider to size up the capital we need to set aside for these important things in life and experiences and in this short article I would like to lay out my thoughts about it.

How Inflexible is Our Need for Better Things in Life?

When we do income planning, if our spending is rather inflexible, which means we cannot expect to spend lesser than the amount that we plan, then what we need from our income is rather inflexible.

And the more inflexible is our income need, usually that defaults to… requiring more capital.

If you tell me: “Kyith, I need $2000 a month for some of the stuff that I like in the past, and also some of the things that I fail to experience last time but that I would do when I stop work, and I need every single cent of this $2000, can you tell me how much in capital, the income strategy and how to invest? I want to prepare for 50 years.”

If you need such a sturdy, inflation-adjusted income stream, for such a long income tenure, I would automatically be conservative and use say, a 2.8% safe withdrawal rate to estimate the size of the capital.

That will come up to ($2,000 x 12)/0.028 = $857,000.

“You mean to tell me if I want to make sure I have these better experiences, I need to set aside that much? How come your income strategy is so weak!! I should just look for someone else!”

Well you can go ahead and look for someone else to find an income strategy that recommends you less capital, and get you what you should want.

I am just giving you my technical perspective based on what I know about your wishes. But it is likely they give you some fancy strategy with less capital, but will work only in situations where the market returns, and inflation is more optimistic (good market returns, below average long term inflation).

If you expect “not a single cent less”, then I got to take care of the scenario where even after 14 years, your portfolio went nowhere and inflation is higher than average. Not what others usually help you size up.

But I think most of you don’t think that way.

Spending on experiences are good to have:

- If my portfolio returns are not so good, I will reduce the grade of the experience I spend on. Instead of travelling for 15 days, I will reduce the number of days. Instead of buying such a rock solid computer to play the game I will make do with a less than solid one.

- For some, they may plan to totally do without (but in my opinion, most cannot do that and it is also not healthy to plan like this).

If we are more flexible, we might be able to use a strategy where the income is more volatile, say 5% of the prevailing portfolio value. The capital that we need might be ($2,000 x 12)/0.05 = $480,000.

Much lesser.

The big determination of how much you need is the depth of your wishes.

However, I will make a case that your wishes is more inflexible than flexible.

If your time on earth is limited, and there are things that will bring you joy, then would such experiences or the things that help you experience this be flexible?

I don’t think so.

You would not want to compromise. This what people would refer to as their bucket list or things to check off when they die.

But in a way, we compromise on this because we are open to the idea that our portfolio might not do so well.

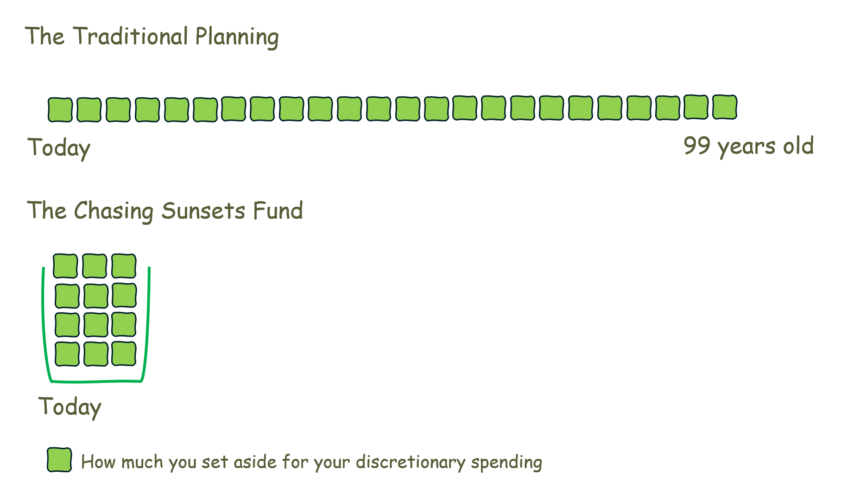

Think of Creating a Sinking Fund to Fund the Most Important Experiences.

What we are limited with is we think that we need to experience this every year for 50-60 years. And due to balancing the trade-offs with other spending today, and saving for the future, we limit our budget. Our retirement income budget is also that way because we don’t know if we will run out of money, so we plan for a limited budget.

If we frame the most important experiences that we collect in your memory, your spouse’s memory, your children’s memory as a few but very rich experiences, then we might not need to plan for the spending to be so recurring.

You would rather experience something nice that you might need to spend $50,000 on instead be limited by your annual budget of $24,000.

Instead of viewing these income needs as a flexible, discretionary spending, extract them and create a sinking fund to make sure you experience them.

That fund can be called:

- Golden Chapter Vault

- Wanderlight Fund

- Passport to Meaning

- Second Bloom Fund

- Moments that Matter

- The Tapestry Fund

- Chasing Sunsets Fund

- Now or Never Fund

I think the names will explain things better than Kyith ever does.

Instead of limited by the constrains of recurrence, focus on what are less non-negotiable, can’t missed out upon and inflexible.

How much to fund a Wanderlight Fund then?

There are a few possible ways to size it up:

- If you already have a list of things that you wish to do, then how much do they cost today? Increase the frequency based on how many times you want to experience them.

- Calculate based on years you want to experience and an annual budget. For example your annual budget is $10,000 and you want to plan for 20 years originally, then it is $200,000

- Out of your current assets, a reasonably significant number that you feel will be adequate to live enough nice experiences.

When I discuss this with my friend, he tells me you can experience a lot of things with $200,000.

I can think of someone that think this isn’t enough. Maybe.

But you should justify to me why that isn’t enough and what is a better number.

Because we are:

- Not ensuring the fund keeps up with inflation.

- Ensuring longevity of the fund.

- Buffering to ensure every year we have adequate to spend on..

We can plan with much less capital than the traditional way.

Moments that Matter Fund helps to Compartmentalize If You are Funding Your Dreams Enough

If you do income planning with an all-in-one income, you will have to mentally think about if you have enough buffers, how much for the basics, for the discretionary.

You end up with so much considerations.

Perhaps my brain is more structural.

I would rather know that even if I spend finish a fund that is called Moments that Matter and it doesn’t compromise the money meant for my future critical care needs, my future medical insurance premiums, or my most essential food.

This is why I prefer a sinking fund concept based around

- The meaning behind the spending needs.

- How flexible/inflexible is the nature of need.

- How long we need it.

- How periodic we will spend from it.

- Does spending need go up exponentially?

Each spending is unique, pivoting around these few attributes.

While this might look tedious, would you rather:

- Worry about if you have enough for your basic spending and so cut down on so called discretionary spending?

- Know exactly an amount specific for the Moments that Matter that is not suppose to cater for your basic spend?

I tend to think #2 requires tracking but may give clarity next time.

What is the Asset Allocation?

This question will eventually pop out if you read Investment Moats long enough.

I think such a fund can finish in 5 years or 10 years, and based on the income needs, it should be predominately fixed income. I think the average maturity matter less but it would be better you keep it less than 10 years to reduce the sensitivity to interest rate fluctuations.

Some of you might want to overfund this amount, make it last longer but you do have to consider the volatility and I tend to think a 40% equity 60% fixed income allocation is more appropriate.

How to Spend from such a Chasing Sunsets Fund?

You tell me how you would do it!

I tend to think if there is something that you feel strong and intriguing about, how would you feel if you missed out? If you think you might feel terrible and you have enough funds for it, then do it.

However, some experiences with the kids might leave a more lasting impression when they are older, and so there might be more considerations.

The idea is not think about doing it every year, but to collect unique ones.

What If You Run Out of Money Prematurely?

I think there might not be a prematurely but that you felt that you want to experience certain things more but not enough money.

That could happen.

The focus of such a fund is to make sure you experience things the normal budget could not and you run the chance the experience is so good that you want to experience that again.

But had you plan the traditional route, you might pander and not even consider the experience at all.

If it is so good, would you go back to work so that you can experience it a few times?

I think some of you would.

I Don’t Have a Name For Mine Yet

Whenever I think about discretionary spending, I would always have in mind that it is a recurring but flexible income fund based around 4-5% of a portfolio value.

More so, I came round to the idea at 45 year old, that planning concept might not be correct.

I should just set aside a fixed sum and just spend it.

I live a prudent enough life and did all the responsible thing and what is left is to spend it.

The name is less important but I do feel that now I see some of the names that I generated with AI tools, meaningful names reminds you why you work so hard to set aside the money and why you need it.

You Might Not Need so Much to Be Happy

I met up with my friend Samuel and he shared with me this:

“Imagine what you know as what you can see when you have a lamp. What you didn’t know, that is beyond what you can see with the lamp might be so, so, so much vast. But to look beyond into the darkness can be pretty scary for some.

If curiosity of what is beyond does not tickle you enough, you can remain in the safety of what you can see in the light. But if you are truly curious about what is out there, it would hurt more if you don’t venture and find out.”

And I guess that is the same with life.

I wonder at our deathbed, do we remember the experiences that we do every year, or would we be more glad we do a few unique things or experiences that are close to heart?

I think it is the latter.

If so, then there might be a flaw in the traditional way of planning. It made us imagine we need to work so much more for it, when with less, we might achieve the same effect.

Let me know what you think about life experiences and how to fund them.

How much would you put in your Chasing Sunsets Fund?

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.